by Daniel | Last Updated July 26th, 2022

We may earn a commission for purchases using our links, at no cost to you.

These days, the convenience of having a credit card can really make your day to day spending habits a breeze, they also present some fantastic value.

And the fact that so many credit card issuers are now offering large sign-up bonuses and a whole range of tempting perks makes them hard to resist.

But there are a few risks that come with owning a credit card that a lot of people don’t know about.

And these things can end up making your life more difficult than it needs to be, with unwanted fees and negative effects on your credit score.

So I thought I would write this article to try and bring more awareness to the potential risks and pitfalls that are involved with owning a credit card, in the hope that you don’t make these mistakes.

1. Closing your Credit Card Too Soon

So a common mistake that some people make is closing a credit card too soon.

And whilst it’s not that hard to actually close a credit card within a short period of time (say 3-6 months) it Is not recommended as it can create more problems than it’s worth.

Generally speaking its worth waiting a full 12 months before canceling a credit card if you feel that it is not

working out for you.

And there are a few reasons why this is important.

The first reason is that if you close your credit card it will immediately affect your total available line of credit, which will affect your credit utilization ratio, and this is something that is used to determine what your credit score is.

Now, something that comes into play here is how much available credit the card has that you want to cancel.

Generally speaking, if the card has a high credit limit of say $30,000 or more, it can make quite a large dent on your available credit if you suddenly close it.

Basically, if you use more than 30% of your available credit on a given credit card, it will not be viewed positively by card issuers or lenders as it is a sign that you may be overextended and are finding it hard to pay off your debt.

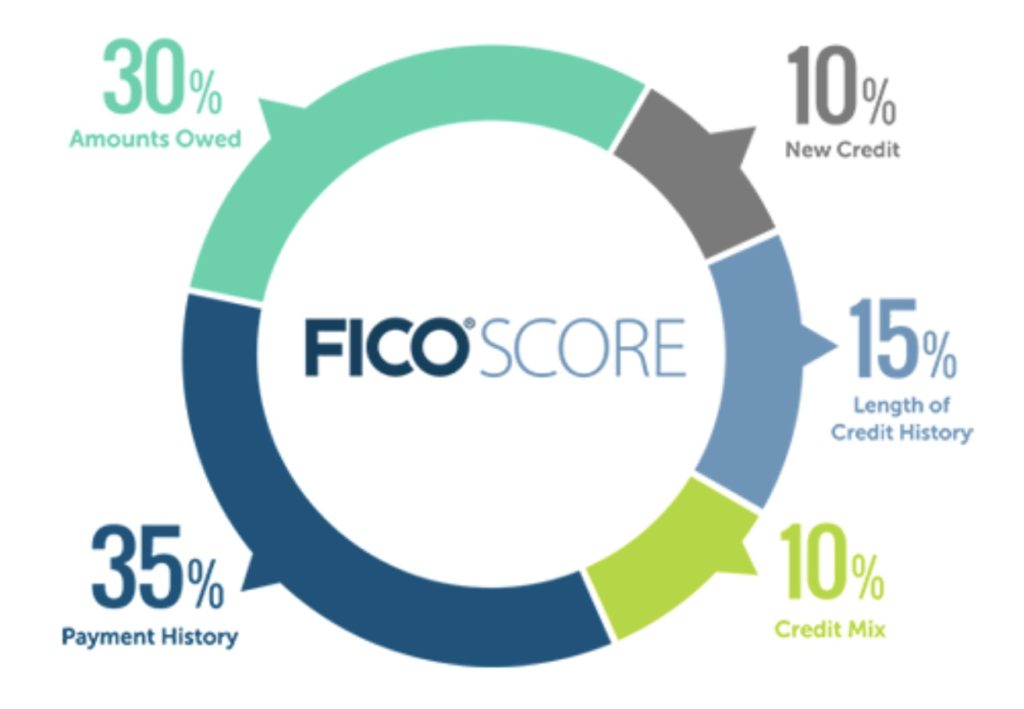

Now another reason that comes into play if you close a credit card is that it will affect the length of your credit history, which is another factor in determining your credit score.

And according to Experion, the length of your credit history accounts for 15% of your credit score.

So if you have had a particular credit card for quite a few years, and have maintained it well, maybe consider looking at a newer card that you have opened recently that doesn’t have as much credit history as your older card.

This will at least help to reduce any negative effects on your credit score.

Now on a side note, if you have a few credit cards and there are one or two cards that you don’t use very often, just make sure to use them occasionally to avoid the card issuer canceling the card due to inactivity, as this would have a negative effect on your credit score.

Other Possible Implications

Now besides the potential negative effect on your credit score from closing a credit card too soon, there is also the possibility of the card issuer canceling your account and not honoring the welcome bonus if they believe that you have misused their credit card just to receive the sign-up bonus.

So it’s really important to read all of the terms and conditions of your credit card.

And a good example of this is written in the Offer terms for the Amex Platinum card.

As you can see in highlighted text, Amex states that they may not credit, may freeze, or take away Membership Rewards Points from your account if you decide to cancel or downgrade your account within 12 months of opening the account.

Wording from the Amex Platinum card terms and conditions:

“If we in our sole discretion determine that you have engaged in abuse, misuse, or gaming in connection with this offer in any way or that you intend to do so (for example, if you applied for one or more cards to obtain an offer (s) that we did not intend for you; if you cancel or downgrade your account within 12 months after acquiring it; or if you cancel or return purchases you made to meet the Threshold Amount), we may not credit, we may freeze, or we may take away Membership Rewards points from your account. We may also cancel this Card account and other Card accounts you may have with us.

Your Card account must not be canceled or past due at the time of fulfillment of any offers.”

So it pays to be careful when applying for any new credit cards by reading all of the terms and conditions, as having the credit card issuer revoke your sign-up bonus, and canceling your account would not be very nice.

Basically, long standing accounts are almost always viewed favorably by credit card issuers and lenders, and will help with your credit history and credit score.

2. Not utilizing The 0% APR Offer Of Your Card

Now, something that you may not about credit cards that offer an introductory 0% APR, is that there is usually a relatively short time period where you can actually make use of the offer.

And this can be for balance transfer or just purchases.

Whilst the terms of different cards are not all exactly the same, it’s really important that you read the fine print in the terms and conditions of the card you are applying for or already have.

As an example, two cards that I recently reviewed which you can read here, both cards offer an introductory 0% APR that runs for 15 months.

With the first card which is the Chase Freedom Unlimited card, the 0% introductory APR has a fee for balance transfers which is either $5 or 3% of the amount of each transfer, but after just 60 days this changes to $5 or 5%, which is a fair bit more, 2% to be exact which can add up.

As an example, if you were to get a balance transfer of say $5,000, it would cost an additional $100 just in fees if you made the balance transfer after the 60-day time period is up.

Then with the second card, which is the Amex Blue Cash Everyday Card, there are only 60 days to actually take advantage of its 0% APR on Balance transfers, after this the APR for Balance Transfers will be between 15.49% to 26.49%, which will end up costing a lot more money if you choose to do the balance transfer after the 60 day period is up.

Now if you do ever decide to take advantage of a 0% APR offer, make sure to work out exactly how much you will need to pay off each month to finalize all payments due by the time the introductory offer has finished.

To do this all you need to do is simply divide the amount you borrow by the number of months that your card has offered you.

So if you did get a balance transfer of $5,000 on a 15-month 0% APR, you will need to pay off approximately $333 each month over the 15 months to be clear of the debt you owe.

3. Only Making The Minimum Required Payment Each Month

Now even though quite a lot of credit card issuers give you the option of making a minimum payment that is due on your balance, it doesn’t mean that it’s a good thing to do.

Generally speaking, by only making the minimum payment each month to your credit card keeps you in debt for a greater period of time, and ends up costing you quite a lot in unnecessary interest charges.

Obviously, if you can’t afford to pay the total owing balance at the end of the month, it is better to make a minimum required payment than to miss a payment altogether.

But, continually paying the minimum amount due can create a mountain of debt that becomes more expensive and harder to pay off as time goes by.

Also, this can greatly affect your credit score if your debt becomes too much, specifically as your credit utilization ratio will become too high and therefore bring your credit score down.

So if at all possible try to pay off your entire balance each and every month to keep yourself out of debt and avoid any unnecessary charges.

4. Trying To Apply For Multiple Credit Cards At Once

Now it’s understandable to want to try and open multiple credit cards, as there are so many great offers available from different credit card issuers.

But it’s worth being cautious as to how often you actually do apply to open a new credit card.

First of all, each time you apply for a new credit card, it’s not uncommon for the card issuer or lender to perform a Hard Inquiry or Hard Pull.

And each hard inquiry will stay on your credit report for 2 years, although most of the negative impact that comes from each inquiry usually passes after 1 full year.

Now this will have a negative effect on your credit score, but it will be different for each individual cardholder depending on what your credit history looks like and what your current credit score is.

Generally speaking, if you have a strong credit history and a great credit score a single hard inquiry for a new credit card should have very little impact on your credit score.

But if you don’t have a great credit history and a poor credit score, it is more likely that there will be a noticeable impact on your credit score.

Now if you suddenly apply for 3 or 4 new credit cards over a short period of time, say 1 month, there will be a much greater impact on your credit score.

When lenders see this many hard inquiries on your credit file within a short time period, It may signal to them that you are experiencing financial difficulties and are at risk of overspending.

According to Experian, it is best to try and wait at least 6 months if not a year before applying for another credit card, as it will greatly reduce the negative effects it will have to your credit score.

So try to keep an eye on how often you do apply for a credit card to avoid any negative impact.

Also, if you are considering getting a mortgage or auto loan, maybe wait until after you have been approved for the loan before applying for a new credit card.

This should help to insure you get a better rate with the lender you chose

5. Getting A Cash Advance

Now getting a cash advance on your credit card is one of the worst things you could do.

Even though it gives you easy access to cash almost instantly, it can create a real problem that will end up costing you a lot in fees and interest payments.

As an example, with the Chase Sapphire Reserve card just to receive a cash advance will incur a fee of either $10 or 5% of the amount of each cash advance, basically whichever amount is more.

So on just a $100 cash advance, the fee would be $10, which is basically the same as a 10% fee.

And then that’s not all, you will start to accrue interest at an APR of 26.49% as soon as you receive the cash.

Then if you take your time to pay back the debt that is owed, it will end up costing you a lot of money.

And then worst of all, if you don’t manage to stay ahead with you’re repayments and fall behind, it is almost certain that your credit card issuer or lender will report this to the different credit bureaus, which will negatively affect your credit score.

So if at all possible, try to avoid using a credit card to get a cash advance, as it will almost certainly save you a lot of money.

6. Making Late Payments

So the last thing that you should never do with a credit card is to miss a payment or make a late payment, as it will end up costing you a lot of money and negatively impacting your credit score.

First of all it is most likely that the card issuer will charge a fee of around $40 each time this happens.

Also most card issuers will then put you on a Penalty APR of about 29.99%.

And each time this happens, it will stay on your credit report for 7 years.

So seeing that your payment history accounts for around 35% of your FICO score, it will almost certainly have a negative effect.

A good way to try and avoid this from ever happening is to set up auto-payments on your account or even just a simple reminder on your phone a few days before your payment is due.

By doing this you should be able to consistently pay off your credit owing, which will result in a better credit score.

Final Thoughts

So that pretty much covers everything I wanted to talk about in this video, and hopefully, it gives you some insight into certain practices that you can use to avoid unnecessary fees and negative effects on your credit score.

Now obviously, every situation is different and it’s not always possible to maintain a perfect credit history, but I hope that this article helps.

Now if you are interested in building your credit score, check out this article here where I basically talk you through the steps required to improve your credit score within 30 days.