by Daniel | Last Updated July 21st, 2023

We may earn a commission for purchases using our links, at no cost to you.

In today’s article, I’m going to show you the ultimate strategy for building your credit score to over 800, and best of all it is free and requires zero skill.

All you need to do is follow the simple steps that I’ll talk you through in this article.

Why Do You Need A Good Credit Score?

So let’s start by answering the obvious question: which is ‘Why do you actually want a good credit score?’

Well, there are several reasons why you would want to have a good credit score.

- The first reason is that you will gain the ability to actually obtain credit from a lender when you need it.

This could be anything from a credit card, auto loan, or mortgage.

Pretty much every lender will look at your credit score to assess what your creditworthiness is.

And the higher your credit score is, the more chance you will have of actually obtaining the credit you need. - Now along with this, it is also more than likely that you will be able to secure lower interest rates on loans and credit cards.

And this is due to the fact that lenders view borrowers with good credit scores as less risky than someone with an average credit score.

This can potentially save you a huge amount of money over the lifetime of things like a mortgage or auto loan.

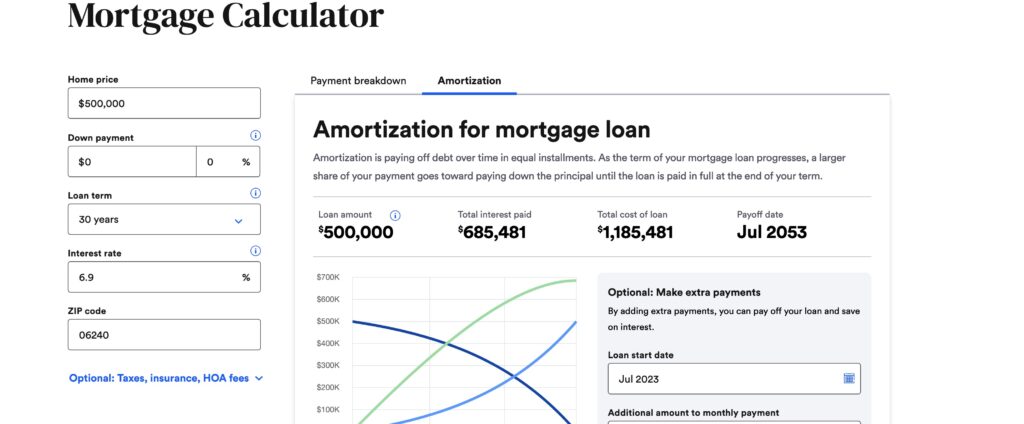

As an example, assuming you have an exceptional credit score of over 800 and you were to get a 30-year fixed-rate mortgage on $500,000 at a rate of 6.9.%, you would be paying $685,481 in interest over this time period.

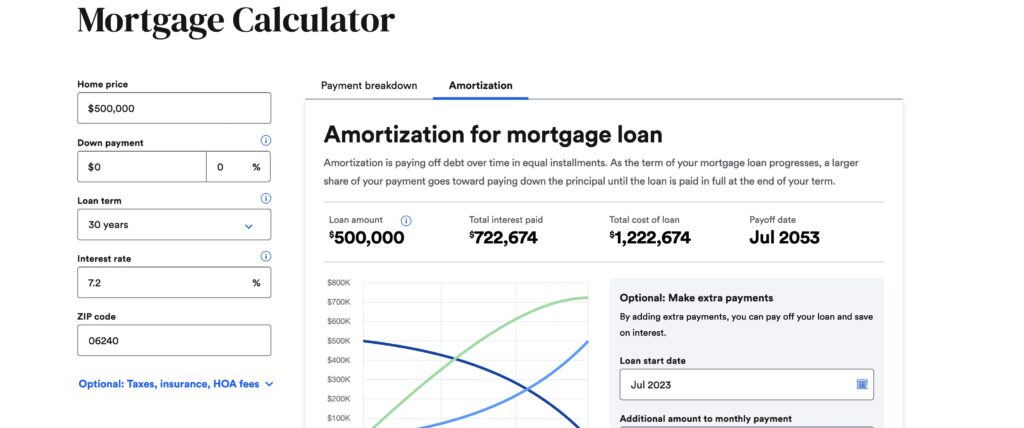

Now if you have a lower credit score of say, 650 you might only be able to get an interest rate of 7.2%, which doesn’t sound that big of a difference, but it will end up costing you $722,674 over the lifetime of the loan, or an additional $37,193.

That’s $1,239 more each year that you will be paying just because your credit score is slightly lower.

And finally, by building and maintaining your credit score you will have access to more opportunities and the financial flexibility to pursue certain goals that require access to credit.

This could be anything from starting a business or expanding your real estate portfolio.

1. Payment history

So let’s start with one of the most critical factors in determining your credit score which is your payment history

This actually accounts for 35% of your overall score, which is more than any other factor.

When lenders or creditors look at your payment history it actually provides them with an extremely valuable insight into how responsible you are with credit, which then provides them with a good idea of your creditworthiness.

How do you manage this?

As maintaining a good payment history is imperative for building a good credit score, here are 4 simple tips you can follow to ensure you keep a good payment history.

- Always pay on time. This is pretty much the most crucial aspect of having a good payment history.

To ensure you do this you must first make sure you have the available funds in your account to cover your bills.

Then you should set a reminder on your phone or computer to notify you to make sure you actually make your due payments.

If this sounds too difficult, you can just set up auto-pay on your account, but like I said before, just make sure you have the available funds in your account to cover the payments. - Make multiple payments. This is an effective way to help keep your credit utilization ratio low (which is something I will talk about later in this video).

It also helps to take away the pain of making one large payment each month.

And it works, I’ve been doing this for years and my credit score has remained over 800 for many years. - Pay more than the minimum required.

This again is a good way to help keep your credit utilization ratio lower, which will positively affect your credit score.

It also demonstrates to lenders that you are actively committed to paying off your debt. - Keep an eye on your credit report.

This is quite important to do as it is possible for there to be errors on your payment history from time to time.

If you do see any issues on your credit report you should report it immediately to avoid any negative impacts it might have on your credit score.

2. Credit Utilization

Now the second most important factor in determining your credit score is Credit Utilization.

This actually accounts for 30% of your overall score, so it is extremely important to be aware of.

Basically, it is a key factor and insight into how you are actually managing your available credit.

it is calculated by dividing what your credit card balance is by your total available credit limit.

If you are able to keep your credit utilization ratio down below 30% or even better, under 10% of your total credit limit, lenders and creditors will consider you to be lower risk and more responsible.

How do you manage this?

Well, one good way is by always paying down your credit card balance on a regular basis.

Another thing you can do is to keep a reminder of what your credit limit is and then try not to exceed more than 30% of this amount.

Now this doesn’t mean you can’t use more than 30% of your available credit limit, it’s just not advisable to have a credit utilization ratio of over 30% for a long period of time.

And this is specifically important for when the credit bureaus check your account which this is generally around the statement date.

During this time, really aim for the lowest credit Utilization Ratio you can manage, anything under 10% would be good.

Length of Credit History

So the length of your credit history is the next important factor that helps to determine your credit score and makes up 15% of your overall credit score.

Basically, it provides a deeper overview of your creditworthiness over time and shows lenders and creditors how you have been able to manage your accounts.

This can include, credit cards, loans, and other lines of credit.

How do you manage this?

Well, this takes time, patients, and constancy.

This is done by always paying off any amounts owing as soon as possible, keeping your credit utilization low, and by avoiding opening too many unnecessary credit accounts.

4. Credit Mix 10%

Now credit mix is another important factor that accounts for 10% of your overall credit score.

Basically, it helps to show your ability to manage more than one type of credit responsibly, which, if done well can positively affect your credit score.

This could include managing credit cards, auto loans, or personal loans in an effective manner.

A good example of a properly managed credit mix would show that you are capable of balancing short-term credit (such as a credit card)with long-term credit (such as a mortgage).

Now if you don’t have a large mix of different credit accounts it shouldn’t really matter to much.

The main thing to remember, as I said before is to pay off all amounts owing on time and to keep your credit utilization ratio nice and low.

5. New Credit

So the 5th and final factor in determining your credit score is new credit, and this also accounts for 10% of your credit score.

This is basically a reflection of your recent credit habits and helps lenders to see if you pose any risk to them.

When you apply for new credit, it can have both positive and negative implications on your credit score.

As credit card inquiries can stay on your credit report for up to 2 years, applying for multiple credit cards in less than 12 months can sometimes lower your credit score as it will basically reduce the average age of your accounts.

How to get started

Get A Secured Credit Card

Now if you’re starting from scratch or are trying to rebuild your credit a secured credit card can be quite helpful.

They are literally designed to help people with limited credit history or poor credit scores build and maintain a better credit score.

The first thing to know is that they are generally easier to get approved for than normal credit cards as they almost always require a security deposit as collateral.

This helps to greatly reduce the amount of risk the card issuer or lender is subject to.

Now the cash deposit required for a secured credit card can vary quite a lot, but it’s not uncommon to see anywhere from $200 all the way up to $5,000 or more.

This money will be placed into a savings account by the card issuer or lender and in return they will give you a similar credit limit.

And this provides the lender or card issuer with the ability to recover any money that the borrower potentially doesn’t pay back.

Now if you do get a secured credit card it is extremely important that you use the card responsibly by making on-time payments, this is because the card issuer will report your payment history to the credit bureaus.

If you continue to be consistently responsible with your secured credit card, your credit score will eventually go up, then you will be presented with better credit opportunities, which will be lower interest rates and better credit cards.

Ways to speed up the process

Become An Authorized User

Now if you’re finding that you can’t wait to get your credit score moving higher it is possible to speed things up by becoming an authorized user.

This basically requires you to find a friend, family member, or just someone that is willing to add you to their account.

And assuming they have a good credit history and make on-time payments, it is possible for you to essentially piggyback off their account and benefit from their positive credit management and good credit score.

Now although this sounds great you must make sure that the account that you choose to be added to actually has a good credit score, low credit utilization, and a good history of making payments on time.

If for any reason the primary account holder misses a payment or uses their credit card in an irresponsible way, it could have a negative impact on your credit score.

So if you do choose to use this method of building your credit score it would be a good idea to contact the lender or credit card issuer of the card you want to be added to and make sure they actually report all of the information regarding the credit card to all three of the major credit reporting agencies which are:

This is really important to do because if they don’t report this information to these credit reporting agencies your credit score won’t improve at all.

Ask For A Credit Limit Increase

So another way of potentially increasing your credit score is by applying for a credit limit increase from your lender or card issuer.

What this does is effectively lower your credit utilization ratio as you are increasing the amount of available credit on your credit card.

Now an easy way to get a credit limit increase would be to read this article here.

So if you are thinking about applying for a credit limit increase just know that it can result in a hard inquiry on your credit report which may negatively affect your credit score for a few months.

Also, if you do decide to do this, make sure you continue to stay on top of your repayments and try to keep your credit utilization ratio nice and low.

Things to Avoid

Making Too Many Credit Inquiries

So now that you have a better understanding of how to build your credit score and how it is actually determined, let’s go over a few things that you should try to avoid.

The first is making too many credit inquiries in a short period of time, as every time you make a new credit inquiry it is recorded on your credit report, and if it is a hard inquiry it can stay there for up to two years.

Now we need to understand exactly what a hard injury is and what a soft inquiry is.

What is a Soft Inquiry?

So a soft inquiry would be anything like checking your own credit score or authorizing a potential employer to check your credit report.

And as both of these examples are not a new application for credit, they shouldn’t have any effect on your credit score.

What is a Hard Inquiry?

Now with a hard inquiry, you need to be a lot more careful about how many times you get one.

Basically, each time you apply for a new line of credit from a creditor or lender they will make a request to view your credit files to see if you pose any risk to them as a borrower.

This will then show up on your credit report and stay there for up to 2 years.

Now just one hard inquiry isn’t the end of the world and usually only causes a small dip in your credit score that lasts for a few months.

But having multiple hard inquiries in a short period of time can substantially lower your credit score.

Final Thoughts

Ok, so that covers pretty much everything you need to know to help build your credit score to over 800.

And generally speaking, it’s not that difficult to do, just make sure you continue to be consistent with your repayments and try to keep your credit utilization ratio as low as possible.

By doing this you can save yourself a huge amount of money over time and even open up more opportunities for better credit and financial products in the future.

Now if you’re looking for a good starter credit card check out this article here where I review the new Chase Freedom Rise credit card.